A Senior iGaming M&A & Strategy Report | February 2026

The iGaming market of Latin America has passed an irretrievable border. Brazil The most predicted regulated market in the region is now fully functioning in the federal controls, Colombia is in its second decade as the regulatory standard in the region and Mexico has a maturing frame that is making its operators have long-term strategic choices and not short-term ones. Latam The waiting and seeing days in LATAM are past.To operators, investors, and affiliates from the 2026 market entry perspective, the question to ask is not whether to enter LATAM, but how and in what structural vehicle.

The White Label paradigm, which has always stood as the entry mode of undercapitalized operators with low friction, is facing real existential threats. This report was commissioned to fill a particular and pressing gap in the strategic intelligence available on the market: most analyses of WL circulating in the market have been authored prior to the federal structure coming into operation in Brazil, prior to the advent of PIX parcelado in the payment ecosystem, and prior to the 2025-2026 shift to Crash Games and social-mechanic products changing the GGR mix fundamentally. The above analysis is no longer serviceable.

What is coming on will be a five-module strategic outline of any player putting up $100K to 8M+ to the LATAM iGaming sector in 2026. It is composed in the financial discipline needed to fit an M&A due diligence scenario, based upon the current regulatory reality, and intended to be put into effect immediately. This report has structures, cutoffs, and decision trees which are made to fit the market as it is today, not as it was when the last wave of WL providers produced their marketing decks.

A note on scope: this analysis deliberately addresses the full spectrum of entry models — White Label, Turnkey, Crypto-Native, and Social/Telegram — because the most dangerous strategic error in 2026 is selecting a vehicle based on familiarity rather than fit. The iGaming industry has a well-documented tendency to default to WL as the “safe” choice. In the current LATAM environment, that default assumption warrants serious scrutiny. Understanding the most common mistakes new casino operators make before committing capital is no longer optional — it is the minimum standard of pre-launch diligence.

MODULE 1: THE WL LANDSCAPE (2026)

WL Viability: Brazil vs. Colombia

Brazil’s Medida Provisória 1.182 framework, now fully operational under SECAP/MF oversight, has fundamentally reshaped what it means to operate a White Label in the region’s largest market. Colombia under Coljuegos remains the region’s most mature regulated environment, now entering its second decade of formal licensing.

| Dimension | Brazil (SECAP/MF) | Colombia (Coljuegos) |

|---|---|---|

| Regulatory Requirement | Federal license mandatory; BRL 30M (~$6M USD) authorization fee | License fee ~$700K USD + annual renewal |

| WL Operator Status | Sub-licensee model allowed under licensed anchor | Must hold direct Coljuegos authorization |

| GGR Tax Burden | 12% CSLL + 15% IRPJ + 18% ISS/PIS/COFINS blend ≈ ~40-42% effective tax | 17% gross revenue tax to Coljuegos |

| KYC/AML Mandate | CPF-linked, COAF reporting, real-time BACEN monitoring | SIPLAFT integration mandatory |

| WL Provider Viability | HIGH complexity; only licensed WL shells viable | MEDIUM; established providers (SoftSwiss, EveryMatrix) already compliant |

| Time-to-Market (WL) | 9-14 months (compliance-gated) | 4-6 months |

| Recommended WL Profile | Capitalized operator >$2M USD runway | Operator $500K-$1.5M USD runway |

Key Insight: Brazil has effectively killed the “plug-and-play” WL model. In 2026, you are not buying a WL product — you are buying access to a licensed operator’s regulatory umbrella, which creates a fundamentally different commercial relationship and risk allocation. Navigating the full landscape of gaming licenses for online casinos is now a foundational competency, not a back-office function.

How WL Providers Handle LATAM’s High GGR Taxation

The tax burden is the central commercial problem. A 40%+ effective tax rate in Brazil means that at a standard WL revenue share of 30-35% of NGR passed to the platform, an operator retains roughly 25-30 cents on every dollar of GGR before any marketing, CPA, or operational cost. The margin math is brutal.

Providers are responding through three structural mechanisms. First, the NGR Pass-Through Model, where the WL provider calculates revenue share post-tax, not on gross GGR — this is now a non-negotiable commercial term for any serious LATAM WL agreement. Second, Tax Entity Pooling, where the anchor licensee aggregates multiple WL sub-brands under a single tax entity, distributing the effective rate across a larger revenue base. Third, Bonus Cost Capitalization, where promotional bonus costs are recognized as deductible operational expenses, reducing the taxable GGR base — a practice SECAP is currently scrutinizing closely.

Grey Market Viability: Curaçao & Anjouan in Argentina & Peru (2026)

| Factor | Argentina | Peru |

|---|---|---|

| Regulatory Status | Provincial patchwork (LOTBA in Buenos Aires); federal bill stalled | MINCETUR framework active but enforcement inconsistent |

| Curaçao License Acceptance | Grey market operational; payment processing increasingly difficult | Grey market viable; PSP options shrinking YoY |

| Anjouan License Value | Marginal — primarily for PSP gateway approvals | Marginal |

| PSP Access with Grey License | Crypto rails + local acquirers via intermediary; card success rates 15-25% | Similar; Niubiz and Izipay domestically difficult to access |

| Player Legal Exposure | None currently | None currently |

| Operator Risk Level | MEDIUM-HIGH; provincial enforcement sporadic but escalating | MEDIUM; MINCETUR C&D letters to grey operators increasing |

| 2026 Verdict | Still viable but window closing — 18-24 month runway estimated | Still viable with lower enforcement risk than Argentina |

The Curaçao 2023 framework reform (OGC licensing) has added a compliance layer that paradoxically makes Curaçao slightly more credible with payment processors, but the fundamental grey market risk profile in Argentina and Peru remains unchanged. Operators entering these markets now on grey licenses must architect an exit strategy toward local regulation or face stranded infrastructure investment. The broader opportunity set across emerging casino markets makes LATAM’s grey zones strategically interesting but structurally transitional.

MODULE 2: THE “LOCALIZATION OR DEATH” SUITE

Payment Infrastructure: PIX & SPEI as Non-Negotiable WL Requirements

This is no longer a differentiator — it is a baseline. Any WL provider that does not offer native PIX integration (via direct BACEN API or licensed intermediary) and SPEI rails in Mexico is not a viable LATAM partner in 2026, full stop.

| Payment Rail | Market | Integration Type | Conversion Impact | WL Provider Standard? |

|---|---|---|---|---|

| PIX | Brazil | Instant; 24/7; CPF-linked | +35-45% deposit conversion vs. card | Mandatory from Tier-1 providers |

| PIX Parcelado | Brazil | Installment PIX (2025 rollout) | Emerging; high LTV signal | Early adoption phase |

| SPEI | Mexico | Instant bank transfer | +20-30% vs. card alternatives | Mandatory from Tier-1 providers |

| OXXO Pay | Mexico | Cash voucher | Critical for unbanked segment (~35% of market) | Standard |

| PSE | Colombia | Bank transfer | Standard; lower friction than legacy | Standard |

| Crypto/USDT | Argentina, Venezuela | Wallet-to-wallet | Essential in hyperinflation markets | Offered by ~60% of providers |

The critical nuance on PIX: because Brazilian regulation now mandates CPF linkage on all financial transactions above BRL 200 (~$40 USD), PIX integration is simultaneously your payment rail AND a significant component of your KYC/AML stack. WL providers that have architected this correctly reduce KYC drop-off rates by 18-28% compared to document-first flows.

Content Shift: Crash Games, Mines & Localized Live Casino

The content landscape has undergone a structural rotation. Traditional slot-led GGR models are being displaced by social-mechanic games with higher session frequency and lower per-bet stakes but dramatically higher session length. Understanding what volatility means in slots — and how LATAM players respond to variance profiles — is directly relevant to content curation decisions.

| Content Category | GGR Share LATAM 2024 | GGR Share LATAM 2026E | Key Drivers |

|---|---|---|---|

| Crash Games (Aviator, JetX, Spaceman) | 18% | 28% | Mobile-first; social sharing; skill perception |

| Mines / Plinko / Fast Games | 8% | 16% | Low-stake, high-session frequency |

| Traditional Slots | 42% | 28% | Declining; still dominant 35+ demographic |

| Live Casino (Localized) | 14% | 18% | PT/ES dealers; local game shows |

| Sports Betting (integrated) | 18% | ~10%* | *Measured as casino-side GGR only |

The role of RNG certification in iGaming is worth flagging specifically in the context of Crash Games and Mines: LATAM regulators, particularly SECAP in Brazil, are applying heightened scrutiny to provably fair and RNG-certified fast-game content. WL providers must demonstrate compliant RNG certification for every title in the aggregated library, not just the flagship slot catalogue. Separately, the case for custom slot development is becoming commercially credible at scale — culturally resonant original content (football themes, carnival aesthetics, regional iconography) is demonstrably outperforming generic European slot content in LATAM A/B tests.

On Localized Live Casino: Portuguese-speaking and regional Spanish-speaking live dealer studios are now a commercial imperative, not a premium differentiator. Pragmatic Play’s Mega Sizzling Hot Live and Evolution’s live game shows with Brazilian hosts are capturing disproportionate GGR share. Any WL package that does not include aggregated access to PT-localized live tables through an API-aggregator (SoftSwiss Game Aggregator, Slotegrator, Hub88) is leaving 15-20% of potential GGR on the table.

Sportsbook Integration: Why Casino-Only WL is a Failing Strategy

The cross-sell dynamic in LATAM has reached a structural tipping point. The Brazilian market’s dominance of football culture means that a user arriving for sports betting and converting to casino represents a CPA efficiency that pure-casino operators simply cannot replicate. A detailed breakdown of how to start a sportsbook is instructive here — the technical and commercial requirements of a genuine sportsbook integration are substantially more demanding than a casino widget, and the difference in player LTV reflects exactly that investment.

| Metric | Casino-Only WL | Integrated Casino + Sportsbook WL |

|---|---|---|

| Blended CPA (paid acquisition) | $45-80 USD | $25-45 USD |

| LTV Month 6 | $90-130 USD | $180-280 USD |

| Session Frequency (weekly) | 2.8x | 4.9x |

| Cross-sell Rate (Sport → Casino) | N/A | 38-52% of sports depositors |

| Churn Rate (Month 3) | 68% | 41% |

| GGR Margin per Active User | Lower | ~2.1x higher |

The implication is clear: in the Brazilian and Mexican markets specifically, a casino-only White Label in 2026 is a deliberately handicapped business model. The WL providers that offer genuinely integrated sportsbook (not just a widget from a third-party aggregator with separate wallets) are commanding a 15-25% premium on their platform fees, and that premium is justified by the LTV data.

MODULE 3: PROS & CONS (FINANCIAL FOCUS)

The White Label P&L Reality in 2026

PROS

| Advantage | Detail | Quantified Impact |

|---|---|---|

| Speed to Market | 6-16 weeks from contract to soft launch (vs. 12-24 months for turnkey/own license) | Critical in fast-moving regulated windows |

| Shared Compliance Infrastructure | KYC/AML, responsible gambling tools, regulator reporting handled at platform level | Saves $200-400K USD in Year 1 compliance build |

| Technical Redundancy | CDN, uptime SLAs, game aggregation, payment routing maintained by provider | Avoids $80-150K USD/year DevOps cost |

| API-Aggregator Access | Instant access to 5,000-10,000+ titles via pre-negotiated aggregator agreements | Achieves in weeks what takes 18+ months of direct negotiations |

| Regulatory Umbrella | In jurisdictions allowing sub-licensee models, significant reduction in licensing capex | Saves $500K-$5M+ in direct license costs |

CONS

| Disadvantage | Detail | Quantified Impact |

|---|---|---|

| Revenue Share Erosion | Platform fee 25-40% of NGR; after tax and WL fee, operator margin can compress below 15% | Structural ceiling on business value |

| Zero Brand Equity / IP | Brand, player database, and tech stack belong to or are dependent on provider | Exit/sale value severely limited; acquirers apply 40-60% discount to WL operators |

| Platform Dependency Risk | Provider insolvency, license withdrawal, or fee restructuring = business destruction | Existential risk with no contractual protection in most WL agreements |

| The 2026 Hidden Fees Problem | See below |

The 2026 Hidden Fee Stack — A Critical Warning

The WL market has evolved a layered fee architecture that was not standard three years ago. Operators must now underwrite these costs in their business models:

| Fee Category | Typical 2026 Structure | Annual Cost Estimate ($500K GGR op.) |

|---|---|---|

| AI Retention Tool Surcharge | $0.50-2.00 per active player/month OR 2-4% NGR uplift fee | $8,000 – $24,000 |

| Responsible Gambling Tech Fee | Mandatory in BR/CO; $0.10-0.30/player/month | $3,000 – $9,000 |

| Payment Routing Premium | PSP failures rerouted via provider’s preferred PSP at +0.8-1.5% per transaction | $12,000 – $30,000 |

| Compliance Update Fees | Regulatory change implementation billed per jurisdiction update | $5,000 – $20,000/event |

| Data Portability Lock-in | Player data export/migration fees upon contract termination | $15,000 – $75,000 one-time |

Total Hidden Fee Impact: In a $500K GGR operation, hidden fees can represent an additional 8-16% GGR drag beyond the headline revenue share, compressing operator NGR margins from a modeled 30% to an actual 14-20%. Well-structured casino bonus mechanics can partially offset churn-related losses, but bonus cost is itself a taxable GGR line item under Brazilian regulation — making promotional strategy a tax planning exercise as much as a marketing one.

MODULE 4: THE ALTERNATIVES

Turnkey Solutions: The GGR Breakeven Threshold

The fundamental question is when the economics of owning your own infrastructure and license justify the capital expenditure and operational complexity. Building a complete iGaming brand from the ground up is no longer purely a technology project — it is a regulatory, commercial, and brand architecture undertaking. Based on 2026 market data across Brazilian and Colombian operators:

| Parameter | White Label | Turnkey (Own License) |

|---|---|---|

| Setup Capex | $50K – $150K | $800K – $3M+ (Brazil: $6M+ license fee alone) |

| Monthly Opex | $15K – $40K | $80K – $200K |

| Platform Fee (% NGR) | 28-40% | 0% (own infrastructure) |

| Compliance Cost | Included in platform fee | $200K – $500K/year |

| Breakeven vs. WL Model | Baseline | ~$3.5M – $5M monthly GGR |

| Asset Sale Multiple | 1.5-2.5x annual NGR | 4-7x annual NGR |

The Breakeven Analysis in Plain Terms: An operator running $4M monthly GGR on a WL model paying 35% NGR share is contributing approximately $1.4M/month to the platform provider. At that scale, the annualized “platform tax” of ~$16.8M/year more than funds the one-time capex of building owned infrastructure within 18-24 months. The inflection point for a serious LATAM operator to initiate a turnkey transition conversation is crossing $2M monthly GGR on a sustained 6-month basis. The slot certification requirements that apply to an owned platform are substantially more demanding than the aggregated certification managed by a WL provider — factoring this compliance cost into the turnkey capex model is essential.

Crypto-Native Casinos: USDT-Wagering in High-Inflation Markets

| Factor | Argentina | Venezuela | Brazil | Mexico |

|---|---|---|---|---|

| Inflation Context | ~120% annual (2025 avg.) | Hyperinflationary; USD de-facto currency | 4-6% (stable) | 4-5% (stable) |

| USDT Adoption | Very High — wallet penetration >35% adults | Very High — survival mechanism | Low-Medium | Low-Medium |

| Crypto Casino Viability | HIGH — players actively prefer USD-pegged wagering | HIGH | Low regulatory tolerance | Moderate grey market |

| Regulatory Risk | BCRA restrictions on crypto; operator risk, not player risk | Minimal enforcement capacity | SECAP explicitly excludes crypto operators from licensing | CNBV monitoring; enforcement inconsistent |

| Recommended Structure | Curaçao/Anjouan licensed; USDT + TRON rails; no local banking touch | Same; plus BEP-20 support | Not recommended in regulated layer | Grey market with low brand profile |

The operational blueprint for how to start a crypto casino in 2026 has materially evolved from even 18 months ago. The key structural changes are the emergence of hybrid fiat-crypto platforms (accepting USDT deposits while settling in local currency synthetically), the proliferation of compliant KYC flows for non-custodial wallets, and the growing acceptance of stablecoin wagering among mainstream LATAM players who are using USDT primarily as an inflation hedge rather than as a speculative asset.

Strategic Assessment: Crypto-native operations in Argentina and Venezuela are not an alternative to a legitimate business — they are a specific product-market fit serving an underserved financial need. The risk-adjusted ROI can be compelling ($80-120K initial capital, no platform fees on crypto rails, no PSP dependency), but the operator must accept that they are building a non-transferable business with limited exit optionality.

Telegram & Social Casinos: The Low-Cost Alternative

A proper understanding of what a social casino actually is — and critically, what it is not — is the starting point for any operator evaluating this model. Social casinos operate on a fundamentally different legal and commercial basis from real-money gaming, and conflating the two in strategic planning is a common and expensive error.

| Dimension | Telegram Casino Bot | Social Casino (Free-to-Play) |

|---|---|---|

| Setup Cost | $5,000 – $25,000 | $30,000 – $100,000 |

| Regulatory Exposure | HIGH if real-money; low if token-based | Low (no real-money wagering) |

| Monetization | Direct crypto payments; no PSP needed | IAP, advertising, VIP gifting |

| User Acquisition | Organic Telegram communities; low CAC | Social/meta platforms; moderate CAC |

| LTV Ceiling | Low-medium; high churn | Low; engagement-based |

| Scale Potential | Limited by Telegram ToS enforcement | Limited by conversion to real-money |

| 2026 Verdict | Valid MVP/market validation tool; not a scalable standalone business | Valid brand-building precursor; not a revenue model |

Practical Application: For a first-time operator with limited capital, a Telegram-based crypto casino in Argentina serves as a legitimate market validation mechanism — it tests payment flows, game preferences, and community acquisition at minimal cost before committing to a full WL deployment.

MODULE 5: EXECUTIVE VERDICT

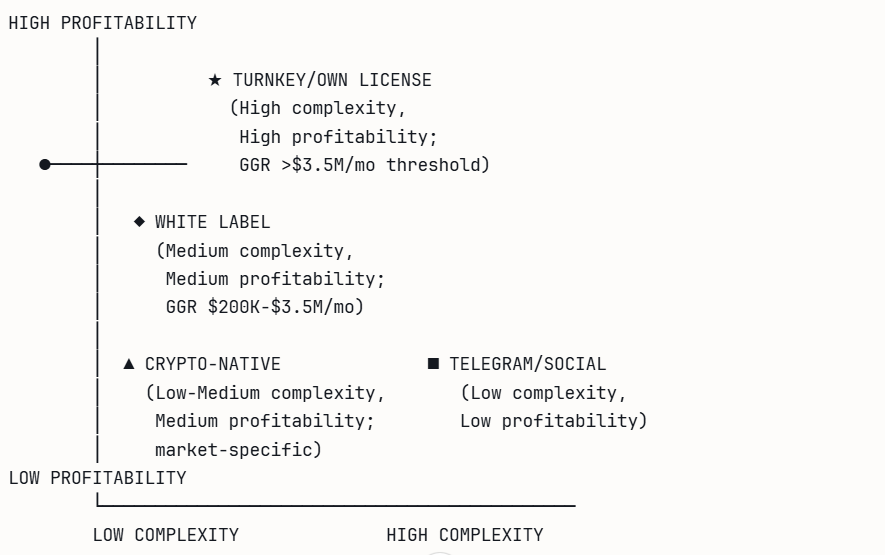

The 2×2 Strategic Matrix: Complexity vs. Profitability

| Model | Complexity (1-10) | Profitability Ceiling | Capital Req. | LATAM Fit Score |

|---|---|---|---|---|

| White Label | 4/10 | Medium (NGR margin 14-22%) | $100K-$500K | 7/10 |

| Turnkey / Own License | 9/10 | High (NGR margin 35-55%) | $2M-$8M+ | 9/10 (scale operators) |

| Crypto-Native | 3/10 | Medium (market-capped) | $50K-$150K | 8/10 (Argentina/VZ only) |

| Telegram/Social | 2/10 | Low | $10K-$50K | 5/10 |

| Integrated WL + Sportsbook | 6/10 | Medium-High (NGR margin 20-30%) | $200K-$750K | 9/10 |

3-Step Strategic Recommendation: The $100K-$250K Affiliate Entering LATAM in 2026

Step 1 — Capital Allocation & Market Selection (Month 1-2)

Do not attempt Brazil as your entry market. The compliance complexity and capital requirements make it a value-destroyer at this capital level. Instead, allocate as follows: with $100K-$250K available, your optimal entry is Colombia or Mexico via a Tier-1 WL provider with integrated sportsbook, or Argentina via a crypto-native/WL hybrid if your affiliate base skews toward that geography. Reserve a minimum of 40% of capital ($40K-$100K) as operational runway — the single most common failure mode at this capital level is undercapitalizing the post-launch acquisition phase.

Select a WL provider (EveryMatrix, SoftSwiss, BetConstruct, or Altenar for sportsbook) that offers: native PIX/SPEI integration, Crash Games content from Spribe/Smartsoft, PT-localized live casino, and a transparent NGR-based (not GGR-based) revenue share agreement. Demand a full disclosure of all surcharges against the hidden fee framework outlined in Module 3 before signing. If you intend to build acquisition via an affiliate programme, understanding how to start an affiliate marketing program from the operator side — not just the affiliate side — is a commercially significant shift in perspective.

Step 2 — Leverage Affiliate DNA as a Structural Advantage (Month 2-4)

Your affiliate background is a genuine competitive advantage at launch. Most new operators buy traffic — you understand how to generate it, qualify it, and negotiate it. Deploy your existing affiliate relationships as your primary acquisition channel for the first 90 days, targeting a blended CPA below $35 USD in Colombia/Mexico. This preserves cash while the product proves its LTV profile.

Set a hard KPI gate at Month 3: if you are not generating $50K+ monthly GGR with a depositor-to-active ratio above 35%, the product or market fit requires correction before increasing acquisition spend. Do not buy your way through a product problem.

Step 3 — The 18-Month Exit or Scale Decision

At the 18-month mark, your business should arrive at one of three outcomes based on GGR trajectory. If you are generating less than $500K monthly GGR, optimize the WL model, reduce provider fees through contract renegotiation (your live data is now negotiating leverage), and consider a market expansion to a second geography using the same infrastructure. If you are generating $500K-$2M monthly GGR, begin the 12-18 month process of scoping a turnkey transition — build the technical and compliance team now, while the WL model funds the build. If you are generating $2M+ monthly GGR, you are at the M&A inflection point: either execute the turnkey transition immediately or engage an iGaming M&A advisor to explore a strategic acquisition by a Tier-1 operator who will pay a 3-5x NGR multiple for a proven LATAM brand with a clean player database.

The White Label Paradox Defined

The central paradox of the LATAM WL market in 2026 is this: the same regulatory maturation that has made WL models more legitimate and bankable has simultaneously made them less profitable. Brazil’s formalization created compliance infrastructure that WL providers can monetize — but the tax burden those same regulations imposed has compressed operator margins to a level where the WL model is best understood as a proof-of-concept vehicle, not a destination business. The operators who will win in LATAM over the next three years are those who use the WL model for exactly what it is worth — speed, learning, and market validation — and who plan their graduation from it from day one.